A Brief Primer on Carbon Accounting

Carbon accounting is the process by which a company quantifies the carbon emissions from its business in order to understand its environmental impact. It is a look back at a company’s emissions footprint from the previous fiscal year.

Terminology

It’s important to clarify terms, since technical details can get confusing fast.

Carbon accounting is also known as a carbon inventory or greenhouse inventory.

The word “carbon” is an umbrella term for atmospheric gasses that are driving the climate crisis, also known as “greenhouse gasses.” These two terms are used interchangeably. But carbon is just easier to say.

In a carbon inventory, seven greenhouse gasses are quantified:

- CO2: Carbon Dioxide

- CH4: Methane

- N2O: Nitrous Oxide

- HFCs: Hydrofluorocarbons

- PFCs: Perfluorocarbons

- SF6: Sulfur hexafluoride

- NF3: Nitrogen trifluoride

Organizational boundaries and emissions scopes

Most carbon inventories follow the accounting framework of the Greenhouse Gas (GHG) Protocol, which separates sources of emissions into three categories: Scopes 1, 2, and 3.

Scope 1: are emissions from owned (or controlled) assets such as company-owned vehicles, trucking fleets, private jets, offices and buildings. These are called “direct” emissions because they are produced from owned assets that combust fossil fuels.

Scope 2: are emissions from energy purchased from, say, a utility to be consumed by your company in the course of doing business. Think: electricity, heat and cooling systems. These are “indirect” emissions because the company does not generate the energy itself, but uses it.

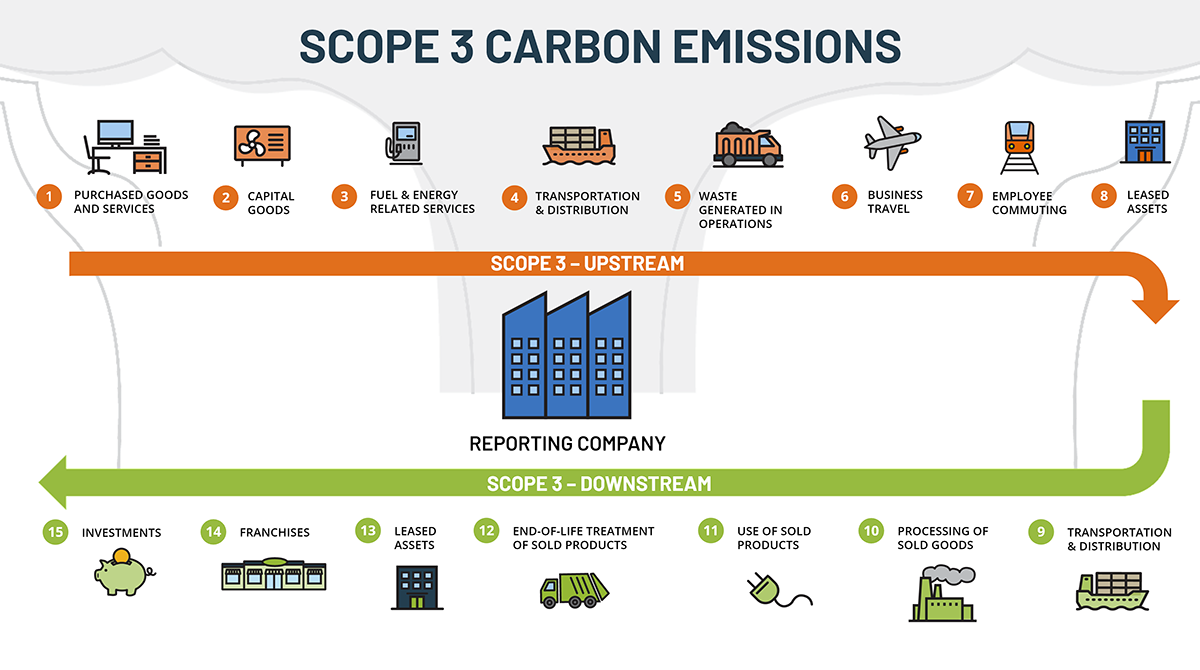

Scope 3: are emissions that occur in your company’s value chain, both upstream and downstream. Think: business travel and employee commuting, purchased goods (manufacturing and non-manufacturing) and services (legal, marketing, consulting), delivery of raw materials to be manufactured, as well as distribution of goods to markets to be sold. Every type of activity that occurs in the course of doing business, except for those defined in Scope 1 and 2, falls into this very large bucket. In fact, Scope 3 breaks down further into fifteen of its own categories, as shown in the graphic below.

Motivations, goals and outcomes of conducting a carbon inventory

Completing a carbon inventory is not uniform across all industries or sectors. No two carbon inventories look exactly the same. For example, no company will calculate all 15 categories of Scope 3 emissions; each company will calculate only the Scope 3 categories that are relevant to their business and operations.

The motivations, goals and outcomes of completing a carbon inventory also vary widely.

Common motivations and goals:

- Comply with climate disclosure regulations, including California bills SB 253 and SB 261 in the U.S. and the Corporate Sustainability Reporting Directive (CSRD) in the EU

- Set and pursue net-zero emissions targets (“what get measured gets managed”)

- Identify opportunities to streamline operations, create new revenue streams, and differentiate the company’s brand

- Meet stakeholder expectations and manage reputational risk

Common outputs or outcomes:

- Including emissions data in a company ESG or impact report

- Declaring metrics to reporting agencies such as CDP

- Disclosing data in SEC filings

- Identifying, executing, and monitoring the most impactful emissions reduction initiatives

- Scenario plan pathways for decarbonizing (moving away from fossil fuel use) operations

- Guide the purchase of carbon offset and/or removal credits

Start your carbon inventory with TripleWin

As a Silver Accredited Service Provider for CDP, TripleWin helps companies improve their environmental disclosures and guide their sustainability strategy from start to finish. We perform carbon inventories for companies of all sizes, public and private, across a host of industries, with a focus on U.S. based companies and multinational affiliates.

Ready to start a conversation about conducting your company’s carbon inventory? Contact us.